REIT stands for Real Estate Investment Trust, so you might be forgiven for assuming that something called a REIT would provide you with exposure to Real Estate.

And generally it does.

A REIT is not a REIT is not a REIT

According to NAREIT (the National Association of Real Estate Investment Trusts), there are 4 different types of REITs:

- Equity REITs: Publicly-traded REITs that own or operate income-producing real estate

- Mortgage REITs: Provide financing for income-producing real estate or purchase mortgages and mortgage-backed securities and earn interest income on these investments

- Public Non-Listed REITs: Registered with the SEC but do not trade on an exchange

- Private REITs: Exempt from SEC registration and do not trade on an exchange

Equity REITs have over 150 publicly traded companies across multiple sectors including:

| * Apartments | * Single Family Rentals | * Data Centers | * Cannabis |

| * Office | * Gaming | * Manufactured Housing | * Farmland |

| * Shopping Centers | * Billboards | * Health Care | * Hotel |

| * Malls | * Self Storage | * Net Lease | * Diversified |

| * Industrial Warehouse | * Cell Tower | * Timber | * Infrastructure |

For a company to qualify for REIT status, it must:

- Invest at least 75% of its total assets in real estate

- Derive at least 75% of its gross income from rents from real property, interest on mortgages financing real property or from sales of real estate

- Pay at least 90% of its taxable income in the form of shareholder dividends each year

- Be an entity that is taxable as a corporation

- Be managed by a board of directors or trustees

- Have a minimum of 100 shareholders

- Have no more than 50% of its shares held by five or fewer individuals

Major Differences

The valuation metrics for Equity REITs is completely different than those for Mortgage REITs.

Mortgage REITs “invest in residential and commercial mortgages, as well as residential mortgage-backed securities (RMBS) and commercial mortgage-backed securities (CMBS). Mortgage REITs typically focus on either the residential or commercial mortgage markets, although some invest in both RMBS and CMBS.”

In addition, Mortgage REITs report “earnings available for distribution” and “book value per common share” while most Equity REITs report “Funds From Operations (FFO)” or “Adjusted Funds from Operations (AFFO)”

But let’s look at it on a sector-by-sector basis.

What does an apartment building have in common with a cell tower? What makes owning an industrial warehouse the same as owning a billboard? How is a timber forest the same as an office building?

.png?width=231&height=121&name=GTT%20Social%20Posts%20Page%205%20(1).png)

Based on the given example, the only similarity between an apartment building and a cell tower is that they are REITs.

An apartment owner/operator has a completely different focus than a cell tower owner/operator. An apartment REIT’s revenue stream is built on the back of its residents monthly rental payment while the cell tower owner’s revenue stream is built on the back of the wireless infrastructure network from such operators as AT&T and Verizon.

Geography is another key element in the puzzle.

For example, is the company:

- Global? (Prologis or American Tower)

- One city? (Rexford Industrial Realty)

- West Coast? (Essex Realty Trust or Retail Opportunity Investment Corporation)

- Sunbelt? (MAA or Highwoods Properties)

- Northeast? (Urstadt Biddle Properties)

- One Tenant? (Postal Realty Trust)

- Suburban? (City Office Trust)

- Skyscraper Office Buildings? (SL Green or Vornado Realty Trust)

- Specialty Office? (Alexandria Real Estate Equities or Easterly Government Properties)

How does a company report revenues/earnings/growth?

- Data Centers: Measured in dollars per watt of power (usually kilowatts or megawatts)

- Apartments: Measured in Revenue per available foot (MRevPAF)

- Hotels: Measured in Revenue per available room (RevPAR)

- Towers: Measured in Total Tenant Billing Growth or Site Leasing

- Malls/Office: Rent per square foot

- Shopping Centers: Rent spreads for new leases on comparable spaces

The long and short of this shows that there are no similarities between REIT sectors and companies as everyone is unique!

Passive REIT Indexes

Let’s look at that passive REIT index. Most of the indexes and index related funds on the market are market capitalization driven which means the holdings would include the largest REITs such as:

- Prologis, Inc. (PLD) – Industrial Properties

- American Tower (AMT) — Cell Towers

- Equinix (EQIX) – Data Centers

- Crown Castle (CCI) — Cell Towers

- Public Storage (PSA) – Self Storage

- Realty Income (O) – Net Lease

- Simon Property Group (SPG) – Malls

- Welltower (WELL) – Health Care

- SBAC Communications (SBAC) – Cell Towers

- Digital Realty Trust (DLR) – Data Centers

- VICI Properties (VICI) – Net Lease Gaming

In this particular example, 20-23% of the average passive REIT Index top-10 holdings is in towers and data center REITs while 20-25% of the top-10 holdings are in “hard assets” such as industrial properties, self-storage units, net lease properties, malls, and casino properties.

Most REIT managers benchmark to the MSCI US REIT Index which shows portfolio weightings to be:

- 24.86% Specialized REITs

- 17.65% Residential REITs

- 16.44% Retail REITs

- 16.23% Industrial REITs

- 10.27% Health Care REITs

- 7.11% Diversified REITs

- 3.67% Hotel & Resort REITs

So in our above example, towers/data centers/infrastructure would constitute almost 25% of the index. Thus an investor is paying fees on 25% of an index that wouldn’t be considered “core” real estate.

And remember that the portfolio is passive and market-cap weighted so on a semi-annual portfolio rebalance, the investor is still holding relatively the same portfolio as before accounting for changes in market caps.

Look at the various passive REIT indexes out there and you’ll notice one thing: THEY ARE ALL THE SAME!

Just because the ETF has REIT in the name doesn’t necessarily mean you are owning the “best” REITs. We have seen too many examples over the past several years of REITs that have gone through issues such as cutting their dividends or filing for bankruptcy “due to market conditions”.

REITs v. Real Estate

Many passive real estate index funds also own holdings such as:

- Weyerhaeuser (WY)

- Rayonier (RYN)

- Jones Lang LaSalle (JLL)

- CBRE Group Inc. (CBRE)

- Zillow Group Class A (ZG)

- Zillow Group Class C (Z)

- PotlatchDeltic Corp (PCH)

- Kennedy-Wilson (KW)

- Cushman & Wakefield (CWK)

- The St. Joe Company (JOE)

- Newmark Group Inc. (NMRK)

- eXp World Holdings (EXPI)

- Compass Inc. (COMP)

- Opendoor Technologies Inc. (OPEN)

- Anywhere Real Estate (HOUS)

- Marcus & Millichap Inc (MMI)

- Redfin Corp (RDFN)

- RMR Group (RMR)

- RE/MAX Holdings (RMAX)

- WeWork (WE)

- Douglas Elliman (DOUG)

- FRP Holdings (FRPH)

- Forestar Group Inc. (FOR)

- Doma Holdings (DOMA)

- Offerpad Solutions (OPAD)

Though these companies are compliments to the real estate industry (such as real estate managers, home marketing services, timber companies, office brokers, etc.) these “non-REIT” holdings add up to almost 6% of the average passive REIT index. If you’re a REIT investor, then why are you exposed to stuff that isn’t REIT focused?

Pure Play?

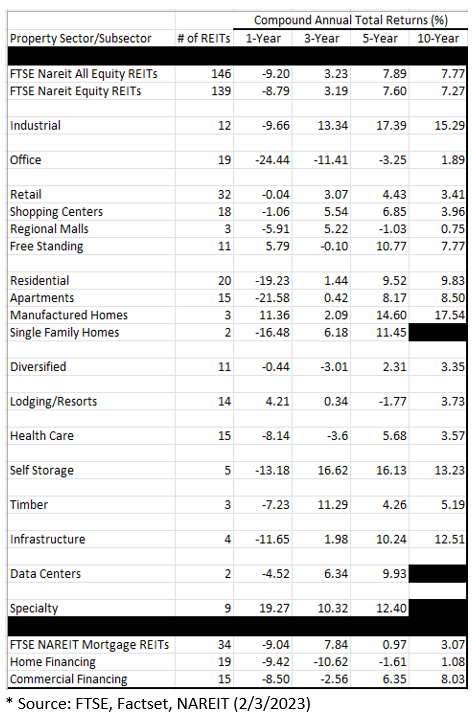

Looking at the NAREIT T-Tracker Index along with the FTSE Nareit U.S. Real Estate Index Series Daily Returns, the data highlights the massive range in performance across multiple REIT sectors and time frames.

Industrial REITs performed poorly in 2022 (down 9.66%) yet over the past 10-years, its compound annual total return is up 15.29%.

Though the 20 Residential REITs declined 19.23% according to NAREIT’s tracker, the individual subsectors are up anywhere from 8.5%-17.54% over the 10-year period (excluding Single Family Rental REITs which haven’t been around as long).

In conclusion, we have shown that no two REITs are alike when it comes to focus, valuation, or earnings metrics. In addition, a passive REIT Index will skew towards higher market capitalization names while other lower-mid capitalization names really never get a chance to shine in the sun. Why play a mixed basket of REITs/Real Estate when you can focus on a pure-play fund that captures the subsector strength?

Performance data quoted represents past performance; past performance does not guarantee future results. Index performance is not illustrative of fund performance. One cannot invest directly in an index. Please call 800-693-8288 for fund performance.

FOR A PROSPECTUS, ADDITIONAL RISKS AND A LIST OF FUND HOLDINGS: https://www.armadaetfs.com/haus/

Through its investments in REITs, the Fund is subject to the risks of investing in the real estate market, including decreases in property revenues, increases in interest rates, increases in property taxes and operating expenses, legal and regulatory changes, a lack of credit or capital, defaults by borrowers or tenants, environmental problems, and natural disasters. The Fund may invest in derivatives, which are often more volatile than other investments and may magnify the Fund’s gains or losses.

The Fund may invest in debt securities which are subject to the risks of an issuer’s inability to meet its obligations under the security; failure of an issuer or borrower to pay principal and interest when due; and interest rate changes affect the prices of fixed income securities. In addition, an increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities.

Distributed by Foreside Fund Services, LLC.

The MSCI US REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs).

The Nareit T-Tracker Index is a quarterly, composite performance measure of the entire U.S. stock exchange-listed REIT industry. Total FFO and net operating income (NOI) for all listed Equity REITs offer a gauge of the industry’s operating performance.

The FTSE Nareit US Real Estate Index Series is a comprehensive family of REIT-focused indexes that span the commercial real estate industry, providing market participants with a range of tools to benchmark and analyze exposure to real estate across the US economy at both a broad industry-wide level and on a sector-by-sector basis.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs

The FTSE Nareit Equity REITs index contains all Equity REITs not designated as Timber REITs or Infrastructure REITs

The FTSE Nareit Mortgage REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. Mortgage REITs

MSCI US REIT Index Data: https://www.msci.com/documents/10199/08f87379-0d69-442a-b26d-46f749bb459b

NAREIT Index Series Daily Returns: https://www.reit.com/sites/default/files/returns/DomesticReturns.pdf